30 Mar 2026 Disruptions to Trade and the Global Economy Due to Iran Conflict – Tea Leaves of Impact of China vs. Taiwan

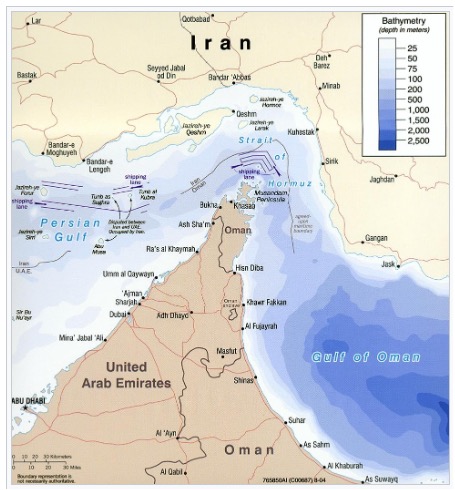

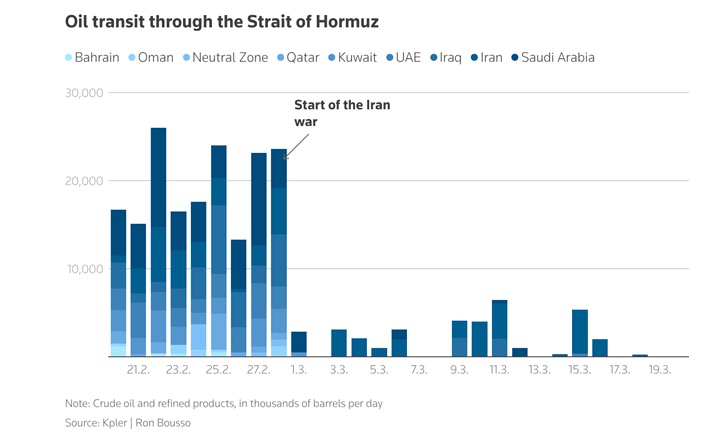

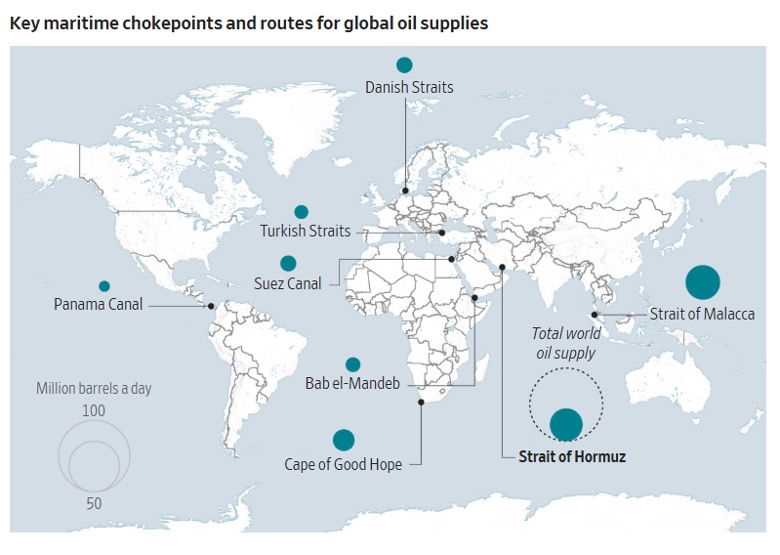

On February 28, 2026, The United States and Israel began striking Iran. Ocean container ship and oil tanker traffic in the Persian Gulf and through the Strait of Hormuz has virtually ceased. The impact of this is increasing price of oil and liquified natural gas (LNG) since 20% of the world’s energy ships from there to the world. Today, 3200 tankers are stranded in the Persian Gulf out of the 8800 tankers in the entire world. There are no major disruptions due to each nation having an inventory reserve detailed in the next paragraph. There is an additional 12 days of global inventory of crude oil in tankers at sea and approximately 10 days more of inventory anchored outside of ports.

Major countries have strategic oil reserves such as Japan with 250 days (99% imported), South Korea with 210 days (99% imported), the United States with 160 days (but produces more than it uses), China with 150 days (70% imported), Western Europe with around 90 days (96% imported) excluding the United Kingdom and Norway which are net exporters, India with 35 days (86% imported), Vietnam with 45 days (57% imported), Thailand with 75 days (80% imported), Indonesia with 24 days (35% imported), Singapore with 30 days (99% imported) , Taiwan with 60 days (91% imported) and Malaysia with 30 days (15% imported).

Many of these countries are already rationing supplies and beginning to implement energy triage as inventories will begin to shrink. Four-day workweeks, switching computers off during breaks, keeping air conditioning at higher temperatures, etc. In a few weeks, energy-intensive industries will begin to curtail manufacturing. These are in addition to major increases in fuel prices.

For countries that have oil production but are unable to load tankers, oil field shutdowns are occurring and will worsen as empty tankers within the Persian Gulf are full.

This Strait is even easier to block than the Strait of Hormuz. First, it is only 500 miles long, and the shipping lane itself narrows to 1.7 miles. Two-thirds of all China trade ships through this chokepoint and 80% of all its imported oil. A few mines or one submarine will close this strait immediately.

It is President Xi’s stated goal to reunite Taiwan with China peacefully, but, if necessary, by force. He has directed the Peoples Liberation Army to be ready to do so by 2027. The consequences are too great to ignore the threat. The West ignored Russia’s threats towards Ukraine. Iran’s threat of obtaining nuclear weapons (to which it has sufficient fuel for at least 11 bombs as claimed by Iranian negotiators in February 2026).

It is President Xi’s stated goal to reunite Taiwan with China peacefully, but, if necessary, by force. He has directed the Peoples Liberation Army to be ready to do so by 2027. The consequences are too great to ignore the threat. The West ignored Russia’s threats towards Ukraine. Iran’s threat of obtaining nuclear weapons (to which it has sufficient fuel for at least 11 bombs as claimed by Iranian negotiators in February 2026).

The time lag for Ukraine to be invaded was very short as was the timeline for attacks on Iran. China will not announce an invasion months in advance.